“The reports of my death are greatly exaggerated”

The text of a cable sent from London to the press in the US by Mark Twain in 1897 after his obituary had been mistakenly published.

A quick google reveals a plethora of articles covering the death of the 60/40 portfolio following Bank of America’s announcement this month.

Whilst there is much more to bdb’s portfolios than simply 60/40, there is no denying that the principles behind holding stocks to provide inflation beating returns and bonds to dampen stock market volatility is a core building block of ours when we consider portfolio construction.

So should we be worried, is diversification dead?

Well forgive me if we don’t start organising the funeral flowers just yet.

The main justification for Bank of America’s (BoA) position is that we are reaching the end of a bond bull market which has helped deliver great returns from those who hold something resembling a balanced portfolio in the last decade. As interest rates have been cut, time and again, bond capital values have risen. In this announcement (BoA) have effectively called the bottom by saying that rates cannot be reduced further. As a result, they conclude that return expectations from the bond part of the portfolio must be lower than they have delivered over the last ten years or so.

The honest answer is we will only know in hindsight.

However, I would say that I have lost count of the number of investment seminars I have attended in the last five years in which this very same prediction for bonds has been made by economists from leading active investment companies (evidence based investors know better than making such predictions). Despite such predictions, rates have continued to fall or flatline for one macro economic reason or another which could not have been foreseen at the time.

Many blogposts and articles offer alternative suggestions to bonds for the portfolio such as increasing equity exposure, overweighting high yielding stocks, gold and even the dreaded structured product rearing its ugly head again. People have short memories don’t they…?

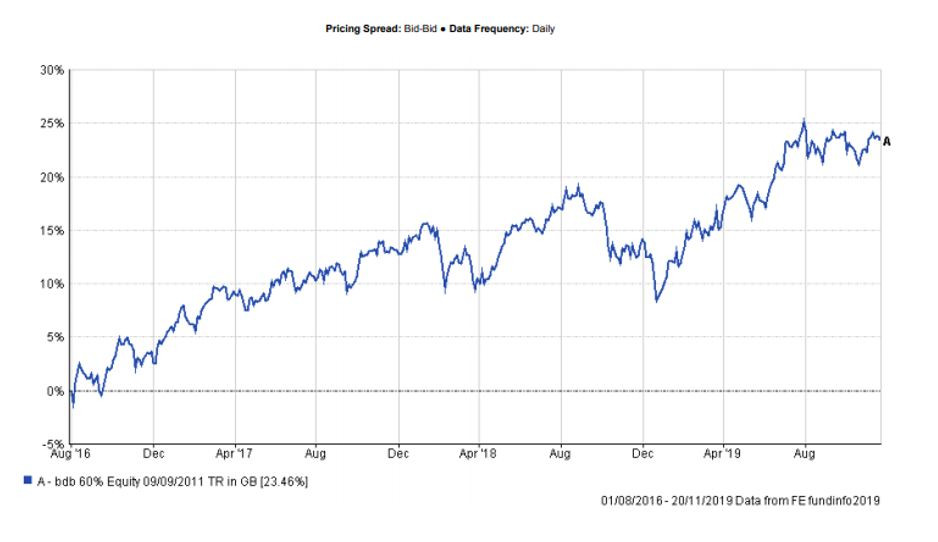

After this months articles disappear off the page, scrolling down the search results reveals a previous article which Mr Twain would have sympathy with. Since this previous ‘death’ in August 2016, our 60% equity portfolio has risen by 23.5%. Food for thought when considering this latest obituary.

In the eyes of evidence based investors such as bdb, the bonds have a specific role as a diversifier and risk dampener in a portfolio. Whilst we are delighted during the periods in which bond returns are strong, this isn’t their primary function. This is why, in our portfolios, the bonds are of the highest quality and tend towards the short end of the maturity spectrum. Risk and return are related after all. As stocks are proven to be the best means of driving return, it makes little sense to take on more risk in the bond piece when you can simply increase your equity exposure relative to your bonds and improve expected returns (i.e. switch to a 70/30).

Being a diversifier means that there is no strong correlation between stocks and bonds. Even if bond returns are not what they have been, equity markets could very well make up the difference. That is after all what diversification is all about.

My challenge back to BoA is if not bonds, then what? Our investment committee has serious problems with some of the alternatives being mooted.

To us this looks like another strategic asset allocation call by an active manager (BoA) which will either be proven right or wrong. Having looked at the stellar returns delivered to diversified investors in recent years, one can forgive the active community for being so keen for it to come to an end. To be honest, it is making them look bad.

Those who know us well will expect it to take a little more to shake our faith in the four fundamental pillars of our investment philosophy which have served us and our clients so well for so long.

Posted by: Matthew Kiddle | Posted in: News