Why do we invest? Well, primarily it is because we want a better return than we would get from leaving the money in the bank or under the mattress.

What is more, there is a very good reason why we should expect a return from investing in listed companies, as we share in the profits of their successful ideas, products and services.

Why do we expect a return greater than our savings account? Well that is because we bear the risk that the companies we invest in may be unsuccessful or even fail.

Risk can be defined in so many different ways. Often it is a quoted statistical measure, such as the volatility of returns, which can sometimes feel abstract. What it really means to us as investors, is uncertainty of outcome. Or, to put it another way, the probability that you don’t get the returns you hoped for at the outset.

Due to the nature of equity market risk, we reduce the uncertainty of the outcome of a well diversified stock portfolio the longer we hold it.

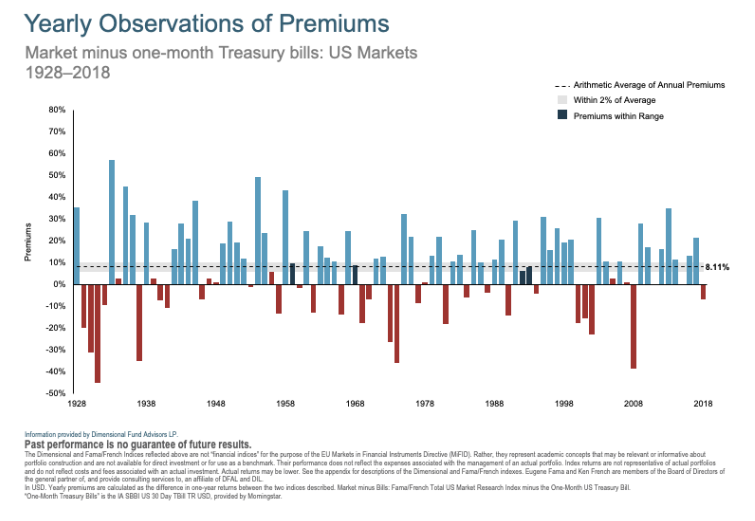

I wanted to share this fantastic chart which captures this really well. I find it so comforting during times when markets do that thing they are doing right now. It shows the difference between cash as measured by one month US treasury bills and US stocks each year 1928-2018 (the story repeats globally, it's just a nice long data set).

You see the return on stocks, over that you would have had from cash, has been fantastic (8.11% per year) if you can afford to be patient (and live for almost 100ish years in this case). Investment markets have done a great job of rewarding investors for their risk.

Nevertheless there will still be those who were just desperately unlucky due to the timing of their investing lives within the sequence of these years. This is risk at work and that uncertainty of outcome in action. Sadly for those individuals, even if they did all the right things, they just got unlucky, such as those in the lost decade of the noughties (sandwiched between two of the best decades on the chart).

The key point one can take from this chart is just how surprisingly spikey it is. Only four of the years shown were “normal” or close to the average of 8.11%. Big ups and downs are actually normal, it's just the price we all pay for the chance of collecting that excess return.

Each drawdown had a different cause whether it be the dot.com bubble, the 2008 financial crisis or 09/11 and each one felt like we were entering a new paradigm at the time. So yes, each has been different in its own way. But when we update this chart at the end of 2020, we will just add another blue or red bar (and 2019s while we are at it) and the chart won’t look much different.

For it to be truly “different this time” 2020’s bar and the conditions which accompany it will need to change the fundamentals of why we invest in equities. It will need to change our belief in capitalism, markets and why we should expect an excess return from investing in companies. None of the crises which have occurred since 1928 managed that, so we’re going to need a LOT of evidence before we start to change our thinking.

Posted by: Matthew Kiddle | Posted in: News