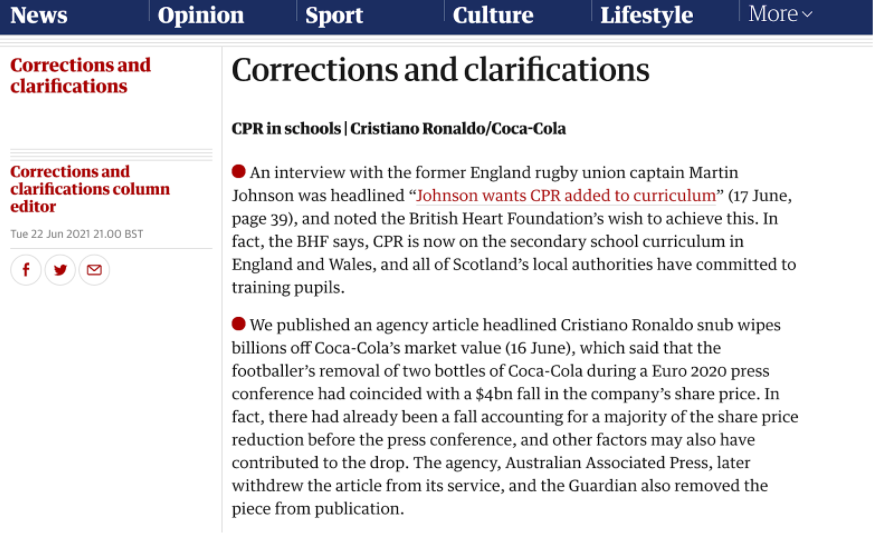

I was interested to listen to the chat amongst my running clubmates on one of the Finance stories of the day last week. Cristiano Ronaldo had reportedly wiped $4bn of value from Coca Cola’s market cap by rejecting the Euro 2020 sponsor’s sweet beverage and stating his preference for good old fashioned H2O in his press conference. You might have caught it on the news at the time.

Interestingly, a search for the Guardian’s article on the subject now reveals only a correction.

It got me thinking about previous articles I had written here about how forward looking and efficient capital markets are and how new information moves prices, not things which are already known or are readily predictable which are already priced in.

Whilst it seemed a big number, perhaps it is plausible that such an action by the most famous footballer on the planet could move a company's share price in this way. We already live in a world where powerful individuals can instantly move markets on their own through their words and actions, see Messrs Trump, Musk and Bezos.

Whilst it made a great story, it looks like a backtrack is now underway and the impact of Ronaldo’s outburst may have been overstated. Yet the story is out and the impact has been made. I would wager my running clubmates will have moved on without seeing the post mortem backtracking and move forward believing the original version of the story.

So what, is that so bad? You might ask

It is human nature for us to look for links or patterns between movements within our portfolios and specific political or economic events. The lesson from the Ronaldo story would seem to be that care is required before attributing causation to any one specific factor, we may have just spotted a timely coincidence.

We need to be aware of our cognitive biases as humans and not oversimplify, the financial markets are vast and complex. At bdb, as you would expect, our investment committee are always looking to further improve our understanding of how the behaviour of wider capital markets and macro economic conditions affects our portfolios.

Whilst we can on occasion confidently link markets to wider world events, we will never lose sight of the fact that in the short term, markets are proven to be impossible to predict.

Posted by: Matthew Kiddle | Posted in: News