Pensions without doubt remain the most powerful long term method of investing. It is the ability to capture tax relief at the very highest rates which makes them so attractive. To harness their full potential it is essential that you make sure you collect all of the tax relief due and I’m a little worried that there are some who are missing out.

This note is aimed primarily at those higher or additional rate taxpayers making pension contributions via their employer. I want to highlight a potential pitfall which can sometimes occur related to how tax relief is awarded on pension contributions. The problem is easily identified if you know what to look for, however if it is not handled properly it can lead to some missing out on thousands of pounds of tax relief and investment return.

So how can you check that your contributions are being handled right?

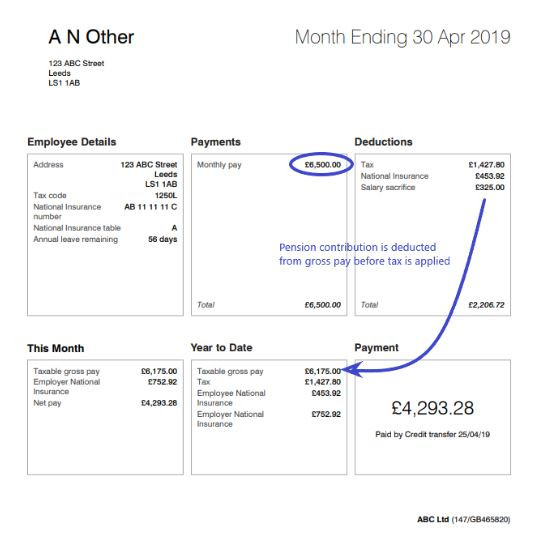

Well the first thing is to see whether your contributions are being dealt with via salary sacrifice. This means that you effectively take a salary cut equivalent to the amount of the contribution you wish to make. Your employer pays it on your behalf (alongside their own contribution) to the pension company. The example payslip below shows how this works with a reduced salary being carried forward into the tax calculation. If this is you, congratulations! You have received all of the tax relief due to you and you can carry on with whatever you were doing before I interrupted you with this post.

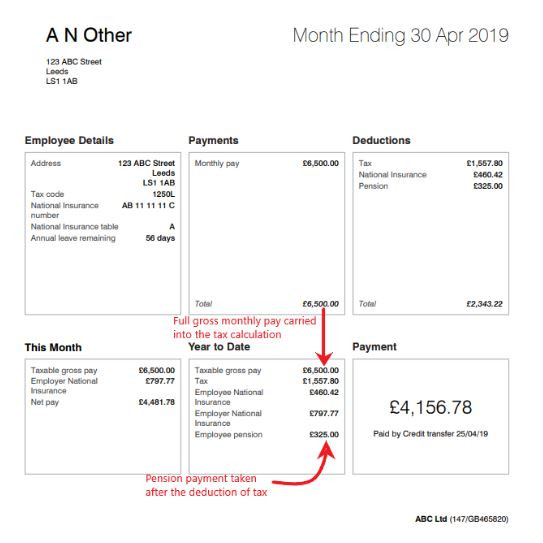

The problem comes where the contribution comes off after the tax calculation (see example below). It is effectively treated the same as making a personal contribution (e.g. writing a cheque from your own bank account). There has been no tax relief awarded via your employer’s PAYE.

In this instance the pension provider will collect the basic rate relief on your pension contribution of 20% and top up your pension account with it. If you are a basic rate tax payer, great news, you too are also now dismissed.

If you are a higher rate tax payer, these gross contributions (the amount you have paid plus the basic rate relief collected by the pension company) must be included in your tax return to collect the higher rate relief. This is exactly the same when you make a personal pension contribution from your bank account.

We have encountered individuals who have been contributing to their pensions via their workplace without understanding the need for this final stage. They were under the impression they were in a salary sacrifice type arrangement. In some cases, they haven’t been submitting tax returns on an annual basis or not including the contributions as they didn’t think they needed to.

By not submitting their contributions on a tax return, they had only been receiving half or even less than half of the income tax relief they were due over a period of years. A sum which would amount to thousands of pounds, not to mention the missed growth on the amount.

If you do spot a problem, don’t panic, the higher rate relief can still be collected. However this will require opening a dialogue with HMRC. Better it is identified quickly and dealt with via your employer. For employers, salary sacrifice is a much neater way of dealing with this and in many cases will eliminate the need for a tax return for your employees.

So the next time you get your payslip just give it an extra glance to make sure you are getting what is rightfully yours.

Posted by: Matthew Kiddle | Posted in: News